ARM vs. Fixed vs. Cash: How Notre Dame Second-Home Buyers Should Pay

Quick Answer

For a second home near Notre Dame, an ARM usually wins if you have a clear 5-to-7-year exit (think four years of student housing), a 30-year fixed wins if you're holding for a decade or planning to retire here, and paying cash wins when you want the strongest offer in a competitive market and don't mind tying up the capital. Your timeline decides more than the rate does.

I've been selling condos and homes near the University of Notre Dame for over 27 years, and I get a version of this question almost every week: "Tim, should I finance this place or just pay cash? And if I finance it, fixed or adjustable?"

Here's what I've noticed. Most buyers walk in already leaning toward whatever their last neighbor or their brother-in-law did. So let me ask you the question I ask all of them first: how long do you actually plan to own this property? Because the honest answer to that question quietly decides almost everything else.

Let me walk you through all three paths the way I'd walk a client through them at my kitchen table.

The Three Ways Notre Dame Buyers Pay for a Second Home

Whether you're buying a game-day condo on Notre Dame Avenue, a townhome for your student for the next four years, or a long-term family retreat near campus, your money flows one of three ways. Here's the 30-second version before we go deep.

| What Matters | 30-Year Fixed | ARM (5/6, 7/6, 10/6) | Paying Cash |

|---|---|---|---|

| Upfront rate | Higher, locked for 30 years | Lower intro rate (fixed 5–10 yrs) | No rate at all |

| Monthly payment | Never changes | Fixed, then adjusts | $0 |

| Rate risk | None | Yes, after intro period | None |

| Best hold period | 10+ years | 3–7 years | Any |

| Offer strength | Standard | Standard | Strongest — fast close, no financing contingency |

| Your cash stays liquid? | Mostly yes | Mostly yes | No — it's all in the property |

Option 1: The 30-Year Fixed (Traditional Financing)

The 30-year fixed is the comfort food of mortgages. You lock your principal-and-interest payment on day one, and it never moves for three decades, no matter what the Fed does. For a buyer who plans to keep their Notre Dame property for the long haul — a retirement landing spot, a multi-generational game-day tradition — that predictability is worth a lot.

One thing to keep in mind: because Fannie Mae and Freddie Mac treat second homes as higher-risk than your primary residence, your rate will already carry a built-in "second-home premium" before you ever pick fixed vs. adjustable.

| Pros | Cons |

|---|---|

| Payment never changes — total budgeting peace of mind | Higher starting rate than an ARM's intro period |

| Zero exposure if rates climb later | You overpay for stability if you sell in a few years anyway |

| Simple to qualify for — underwritten at the actual note rate | Higher payment can pinch cash flow on a rental |

| Easy to refinance later if rates drop | If rates fall, you're stuck until you refinance and pay closing costs again |

Best for: The buyer who answers "how long will you own it?" with "honestly, probably forever." If you want to run real numbers on a fixed payment for a specific property, my preferred mortgage lenders can give you an actual pre-approval, not a guess.

Option 2: The Adjustable-Rate Mortgage (ARM)

An ARM gives you a lower fixed rate for an introductory window — usually 5, 7, or 10 years — and then it begins adjusting with the market. Historically, that intro rate runs roughly 0.25% to 0.75% below a comparable 30-year fixed. On a second home that already carries a rate premium, that discount can quietly put a few hundred dollars a month back in your pocket during the early years.

Here's where the Notre Dame market gets interesting. A huge share of campus-adjacent purchases have a natural expiration date built right in. Your student graduates in four years. Your "we'll do this for a few seasons" game-day plan has a shelf life. If you already know you're likely to sell before the adjustment period ever kicks in, you can pocket the lower rate and walk away before the risk arrives. That's the ARM's whole pitch in this market.

| Pros | Cons |

|---|---|

| Lower intro rate helps offset the second-home premium | Payment can jump once the fixed period ends |

| Lower payment improves cash flow on a rental during ownership | If plans change and you hold longer, you inherit the rate risk |

| Perfect fit for a known 4-to-7-year exit (the "student housing" play) | Often qualified at a higher "fully indexed" rate, so it can be harder to approve |

| Frees up monthly cash to pay down principal aggressively | Requires discipline — it rewards people who actually have an exit plan |

One thing buyers don't expect: lenders don't just check whether you can afford the teaser rate. To protect themselves, they often qualify you at the higher index-plus-margin rate. So if your monthly debts are tight, an ARM can occasionally be tougher to land than a fixed loan. It's worth knowing before you fall in love with the lower number.

Best for: The buyer with a real timeline — four years of school, a planned 5-to-7-year hold, or an aggressive payoff strategy. Curious what you'd actually qualify for? Start with a real pre-approval through my recommended mortgage lenders.

Option 3: Paying Cash — Is It Actually the Smart Move?

I'd say close to a third of my out-of-town buyers ask whether they should just pay cash. It's a fair question, and the answer isn't automatically "yes" the way people assume. Cash buys you something very real in this market — but it costs you something too.

Here's the piece most folks overlook: financing a condo near campus can be genuinely tricky. Lenders scrutinize the HOA's owner-occupancy ratio, reserve funds, and budget before they'll approve a loan on a unit. In a building with too many rentals or a thin reserve, a buyer can get cold feet at the financing stage. Cash sidesteps that hurdle entirely — no appraisal, no lender condo-warrantability review, no financing contingency. In a competitive situation near the stadium, that can be the difference between winning the unit and writing the backup offer.

| Benefits of Paying Cash | Trade-Offs vs. Financing |

|---|---|

| No interest, ever — and no monthly payment | Your capital is locked in an illiquid asset |

| Strongest possible offer: fast close, no financing contingency | You give up leverage — financing lets a smaller amount of cash control the asset |

| Skips the condo-warrantability and appraisal gauntlet | Opportunity cost: that money isn't earning a return elsewhere |

| Lower closing costs — no lender fees | Less liquidity cushion for surprises or other opportunities |

| 100% equity from day one | Concentrates a large chunk of net worth in one property |

Here's the question I'd actually ask you: if you pay cash, what does that money stop doing for you elsewhere? Some buyers genuinely sleep better owning free and clear — and I'd never argue with peace of mind. Others realize they'd rather finance, keep their reserves working, and buy a stronger position. There's no universally right answer; there's only the one that fits your situation. And remember — you can always pay cash now and do a cash-out refinance later, though you'll borrow at whatever rates exist then.

The "Notre Dame Effect": Your Exit Strategy Decides

If you take one thing from this article, take this: near campus, the property often tells you how long you'll own it. Match your financing to that timeline and the rest falls into place.

| Your Situation | My General Lean |

|---|---|

| Buying a condo for your student's 4 years on campus | ARM — you'll likely sell before it ever adjusts |

| Game-day place you plan to keep for decades | 30-year fixed — lock it and forget it |

| Competitive bid on a condo with a tricky HOA | Cash — strongest offer, sidesteps warrantability |

| Future retirement home, want it paid off fast | ARM + aggressive payoff, or cash if liquidity allows |

A Quick Word on Qualifying for a Second Home

Second-home loans are stricter than primary-residence loans, so it helps to know the bar before you start:

- Down payment: typically 10% to 20% down on conventional financing.

- Credit score: often 720+ for the best pricing.

- Debt-to-income (DTI): usually needs to sit under about 43% to 45%.

- Loan type: FHA and VA loans cannot be used for second homes — conventional only.

These are moving targets that depend on the lender, the building, and the day's rates. The fastest way to know your real numbers is a proper pre-approval. You can connect with my trusted local mortgage lenders to get one started — and yes, a pre-approval, not just a five-minute pre-qualification, is what you want before we write an offer.

My Honest Take

After 27 years doing this near campus, I've stopped believing there's one "best" way to pay. The buyers who get this right aren't the ones who chase the lowest rate — they're the ones who get honest about their timeline first and let that drive the decision.

So before you lock anything in, I'd genuinely just ask yourself: what's my real plan for this property, and what do I want my money doing for me over the next few years? Answer that, and the financing question mostly answers itself.

If you want a second set of eyes on a specific property — including whether a particular condo building is even financeable — that's the conversation I have all day. No pressure, no pitch. Where should we go from here? Reach me at 574-329-9587 or Tim@TimVicsik.com, and we'll figure out what actually fits.

Frequently Asked Questions

Is an ARM a good idea for a Notre Dame game-day condo?

It can be an excellent fit when you have a defined exit — for example, buying a condo for your student's four years on campus. You capture the lower introductory rate and typically sell before the loan ever adjusts. If you plan to hold the property for decades, a 30-year fixed is usually the safer choice.

Should I pay cash for a second home near Notre Dame?

Paying cash gives you the strongest offer, a faster close, no interest, and it sidesteps the condo-financing approval process. The trade-off is liquidity — your money is locked in the property instead of earning a return elsewhere. It's a great move for competitive bids and buyers who value simplicity, but not automatically the best financial play for everyone.

What credit score and down payment do I need for a second home in Indiana?

For conventional second-home financing, plan on 10% to 20% down, a credit score ideally around 720 or higher for the best pricing, and a debt-to-income ratio under roughly 43% to 45%. Exact requirements vary by lender and by the condo building itself.

Can I use an FHA or VA loan to buy a Notre Dame condo as a second home?

No. FHA and VA loans are reserved for primary residences and cannot be used to purchase a second home. Second-home buyers use conventional financing, which carries a built-in rate premium compared to a primary-residence loan.

Why is it harder to finance a condo near campus?

Lenders review the condo association's financial health — owner-occupancy ratios, reserve funds, and budget — before approving a loan on a unit. Buildings with a high share of rentals or thin reserves can be flagged as "non-warrantable," which complicates financing. This is one reason some buyers choose to pay cash near campus.

Related Articles

- Buying Near Notre Dame in 2026: Condo vs. House Cost Breakdown

- Browse Notre Dame Condos for Sale Near Campus

- Get Pre-Approved With My Trusted Mortgage Lenders

Thinking about a place near Notre Dame?

Save a few listings, create a free account to track them, and when you're ready, let's talk through the financing that fits your plan. Reach Tim Vicsik at 574-329-9587 or Tim@TimVicsik.com.

Categories

- All Blogs (89)

- Best Time To Sell (9)

- Condos and Villas (21)

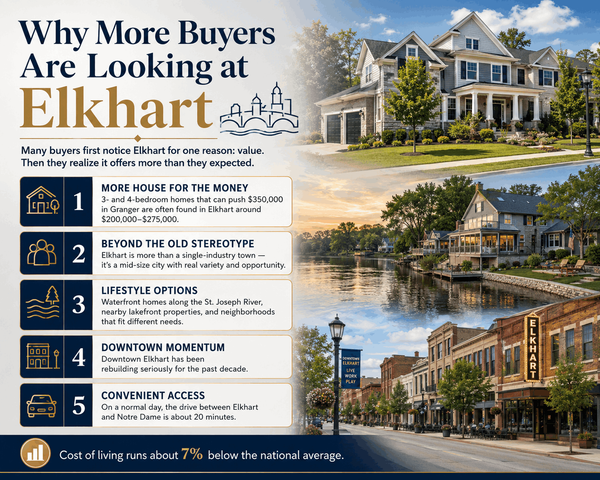

- Elkhart (33)

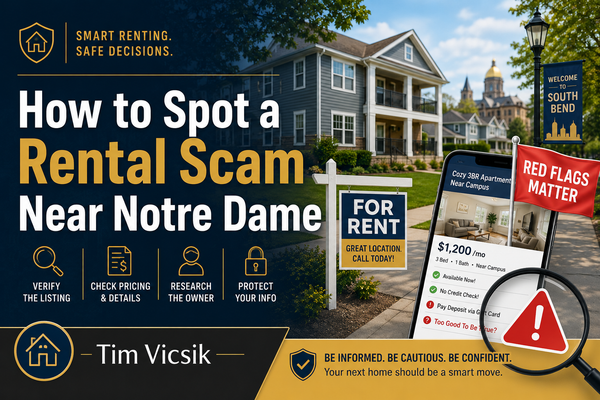

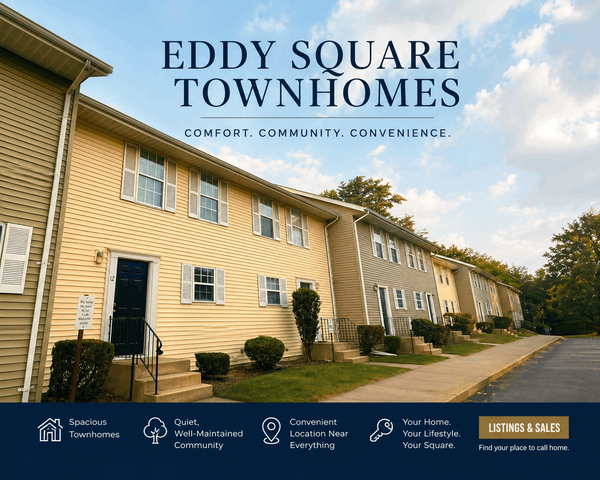

- For Buyers (56)

- For Sellers (29)

- FSBO (13)

- Granger (31)

- Guides (60)

- Housing Market (35)

- Housing Trends (1)

- Inspections (5)

- Lifestyle (9)

- Market Trends (10)

- Mishawaka (31)

- Mortgage (13)

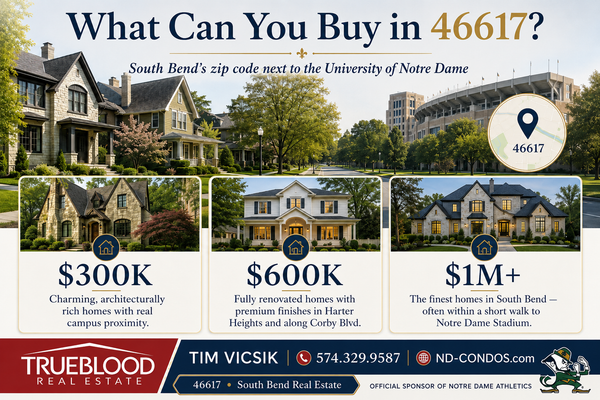

- Notre Dame (60)

- Property Tax (5)

- South Bend (62)

- Things To Do (3)

- Waterfront (1)

Recent Posts

GET MORE INFORMATION